Which European sustainability reporting standard is right for your company?

Between the Simplified ESRS, VSME, Voluntary ESRS, and ESRS-TC, European sustainability reporting has become a maze of overlapping standards. Here's what each one covers — and which one actually applies to your company

Simplified ESRS

Status: Final

What is it: The core standard for EU companies in scope for CSRD.

- The Simplified ESRS includes hundreds of potential data points and requires a double materiality assessment—meaning you must assess both how sustainability issues affect your company and how your company affects people and the environment.

Who it's for:

- Mandatory standard for EU companies in scope for CSRD.

- Wave 1 companies technically have the option to use these standards for their 2027 reporting (on financial years starting on or after January 1, 2026). We recommend moving to the Simplified Standard to avoid unnecessary reporting.

- Other European companies in-scope for CSRD must use these standards in their first reporting year (i.e. 2028).

- Optional for companies not in scope for CSRD but who want to proactively meet customer, supplier, and investor requests.

VSME standard

Status: Final, available for use

What is it: A lightweight, voluntary reporting framework designed as an entry point for micro, small and medium enterprises (SMEs).

- The VSME is designed as an entry point—if your company is new to sustainability reporting and is fielding disclosure requests from banks, investors, or larger customers, this is where to start.

Who it's for:

- SMEs with little or no experience collecting and reporting sustainability data.

- The EU defines SMEs as businesses that have fewer than 250 employees and less than €50 million in revenue or €43 million in balance sheet assets.

Voluntary ESRS

Status: Final

What is it: A voluntary standard for non-SME companies that lost their CSRD reporting obligation after the Omnibus changes

- The Voluntary ESRS are very similar to the VSME standard. If your company is small but above SME thresholds, this is the Commission's intended standard for you.

Who it's for:

- Smaller companies with no sustainability reporting experience that are newly out of CSRD scope.

A note: For companies above €50 million in revenue, we recommend the Simplified ESRS or ISSB over the Voluntary ESRS. The voluntary standard, as currently drafted, won't prepare you to meet the growing volume of sustainability data requests from customers, investors, and regulators. More on this below.

ESRS-TC (formerly N-ESRS)

Status: First exposure drafts published in June 2026, first approved draft expected in early 2027

What is it: A separate set of standards for non-EU parent companies with significant EU operations.

- The ESRS-TC use impact materiality assessments (not double materiality) and contains fewer data points than the Simplified ESRS. The standards only require disclosure of impact-related data, and no sustainability-related risks and opportunities.

- The first exposure draft (draft that will be debated by technical working groups associated with the Commission) of the ESRS-TC was published in June 2026, with a number of further consultations scheduled for 2026.

Who it's for:

- Non-European parent companies in scope for CSRD, formerly known as ‘Wave 4’ companies (mandatory).

- Many of these companies are likely also in-scope for ISSB-aligned regulations. ISSB does require financial materiality assessments, as well as disclosure of sustainability-related risks and opportunities. In some cases therefore, it may be easier for companies to follow the Simplified ESRS in their disclosures to maximize ISSB interoperability.

- Currently, we recommend non-EU companies in-scope for CSRD plan to follow the ESRS-TC in their 2029 CSRD reports. However, will update this recommendation depending on what the final ESRS-TC are.

Why the voluntary ESRS/VSME may not be right for you

If your company has revenue above €50 million, you'll face a steady increase in sustainability data requests—regardless of whether you're technically in scope for CSRD. The Voluntary ESRS won't prepare you for that. For example, the ‘Basic Module’ of the VSME doesn’t require disclosure of Scope 3 emissions, but that is almost always a top ESG issue for companies of any reasonable size.

Two better options:

- The International Sustainability Standards Boards reporting framework is the most widely adopted framework outside the EU. If your company has significant operations beyond Europe, start here.

- Simplified ESRS is the better choice if your operations are primarily in the EU. European stakeholder demand for this data is growing, and reporting against this standard now puts you ahead.

These standards are designed to work together, and interoperability is expected to increase over time. Starting with one won't box you out of the other.

What about the CSRD value chain cap?

CSRD requires reporting companies to collect data from their supply chains and customers. To minimize CSRD data burden on suppliers, the Omnibus agreement introduced the concept of a value chain cap for SMEs. Under the cap, suppliers with fewer than 1,000 employees can refuse data requests that go beyond what the VSME standard requires. You may think that following the VSME standard reduces the burden of future data requests. However, the cap is narrower than it sounds.

The value chain cap limits what companies can request from suppliers specifically for CSRD compliance. It doesn't limit other requests. Your customers and suppliers can and likely will still ask for data beyond the VSME to comply with other regulations (CSDDD, EUDR, EPR) or for their own analysis.

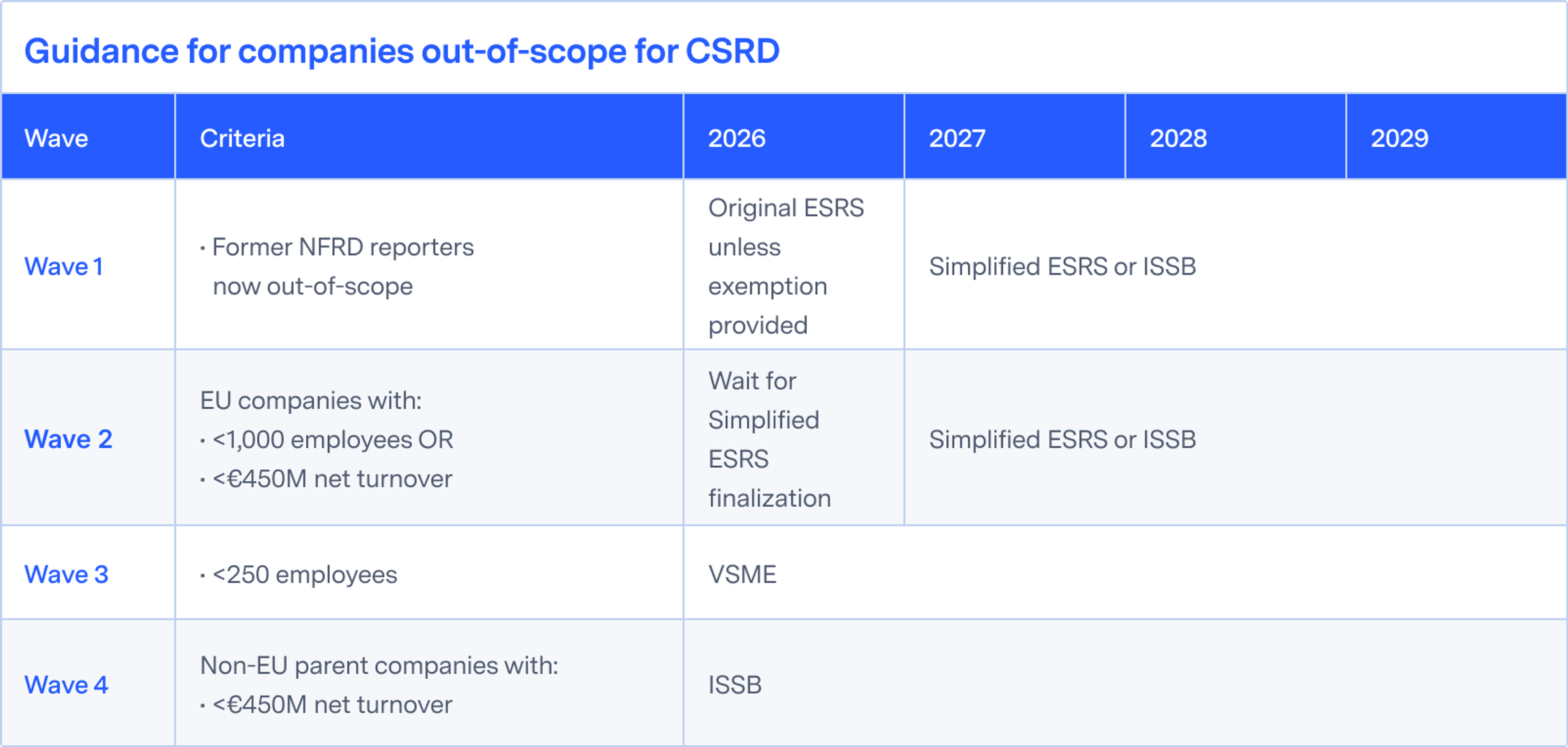

Summary: What standard to follow, and when

The original CSRD organized companies into four reporting waves with corresponding standards. The revised CSRD doesn't use waves, but many companies still think in those terms. Below is guidance for both in-scope and out-of-scope companies organized by waves.

How Watershed can help:

Watershed helps you report against ESRS, ISSB, and other major frameworks from a single platform. Our expert advisory team can help you choose the right standard and build your sustainability report.