The climate crisis demands urgent action, and regulators in the EU and UK are taking strict but critical measures to ensure the private sector does its part. As this surge of new climate legislation can be overwhelming to track, we’ve prepared this guide to summarise the major developments and what they mean for 2023 filings.

Watershed helps companies and financial organisations—like Spotify, Monzo, Klarna, and Baillie Gifford—measure, report, and take action to reduce their emissions. Our in-house team of climate advisors helps customers parse new policies and prepare for their accompanying disclosure mandates. If we can assist with any of these programmes, please get in touch.

Overview

New rules for 2023 filing

Read more about these programmes in this blog post.

- SFDR (EU)

- CRFD/BEIS (UK)

- FCA (UK)

- DWP (UK)

Rules remain the same in 2023

Below are links to more information about the programs that will stay the same, or that don't have filing requirements in 2023.

Programmes

SFDR - The EU’s Sustainable Finance Disclosure Regulation

What it is

As demand for sustainable financial products grows, investors want more data on how investments actually promote sustainability—and on how climate risks may impact their value. SFDR directs financial firms and advisors on how to offer this transparency.

What you need to know

On 6 April 2022, the EU released their regulatory technical standards, or new set of SFDR rules. These rules are often referred to as “Level 2”, as they flesh out what was originally fairly high-level guidance. Two months later the EU also added additional clarifications. These new rules apply from 1 January 2023, covering the next filing date of 30 June 2023.

The key points:

- Any financial product marketed as sustainable must be classified as either Article 8 (partially sustainable) or Article 9 (fully sustainable). See more explanation here.

- Both classifications require the regular disclosure of 14 Principal Adverse Impact (PAI) indicators—ie. metric-based answers to how the underlying investments impact the environment (eg. carbon emissions) and society at large (eg. gender pay gaps).

- These PAI metrics must be inclusive of funds, funds of funds, derivatives, holding companies, and SPVs—which is to say that you have to count everything, all the way down, even if finding or estimating this data is difficult.

- One of these metrics is Scope 3 carbon emissions—ie. your fair share of emissions from portfolio companies. This will be difficult, as many companies are still early in their carbon measurement. Watershed can help with this, and with accounting for all six climate-related PAI metrics.

The EU also updated the rules for the Market in Financial Instruments Directive II (MiFID II). As of 2 August 2022, all EU financial advisors must ask clients about their sustainability preferences. Clients in favour will be pointed to SFDR-aligned products, and provided disclosures that cover those 14 core PAI metrics—including data going back five years.

As investments with poor trending performance will stand out, serious climate action throughout portfolios is now even more of a competitive advantage. For investment managers who want to help their portfolio companies stay ahead of the pack, we can help.

CRFD - Climate Related Financial Disclosures

What it is

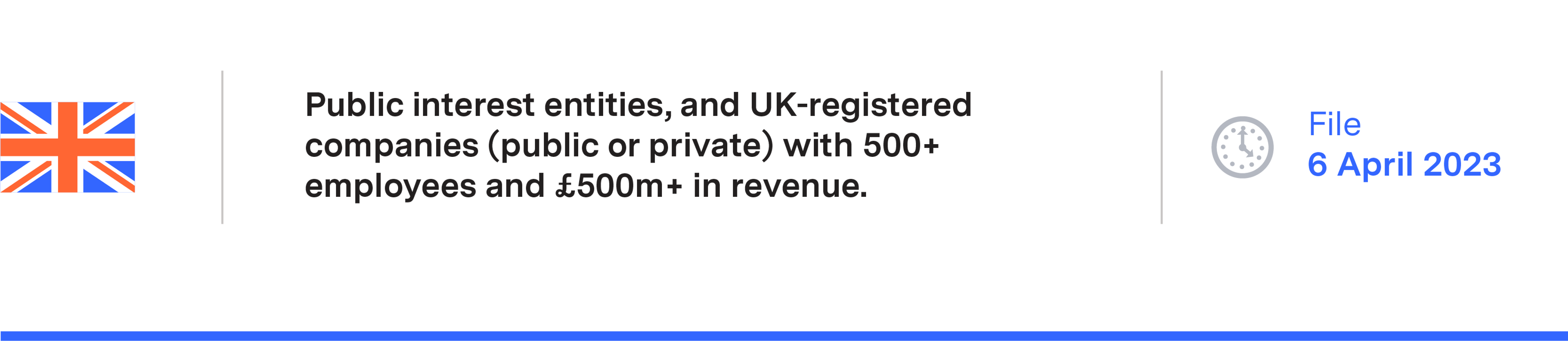

Formerly referred to as BEIS (after the now-restructured Department of Business, Energy, and Industrial Strategy), this reporting regime requires covered organisations—including banks and insurance companies—to include eight sustainability-related disclosures each year. These new rules apply to accounting periods starting on or after 6 April 2022—i.e. all annual reports after that date in 2023.

Note: Companies with a UK parent whose BEIS report already covers their operations are exempt from filing a separate report.

What you need to know

CRFD’s rules are based heavily on the TCFD voluntary standard, which poses 11 considerations that determine if a climate disclosure is thorough enough.

CRFD covers the same substance as TCFD but narrows down to just eight disclosures, each of which references an organisation’s climate-related risks and opportunities:

- What they are

- How they’re handled at a governance level

- How they’re assessed practically

- How they’re integrated into overall risk management

- What their actual and potential impacts are on the organisation

- How resilient the organisation is in various climate scenarios

- Which broad targets are used to manage the risks and realise the opportunities

- Which KPis are used to assess progress against these targets

These answers must then be submitted as part of the organisation’s non-financial and sustainability (NFIS) statement within their Strategic Report, else via the Energy and Carbon Report section of their standard Annual Report.

While there is no specific requirement to disclose carbon emissions, all organisations reporting under CRFD will also be reporting under SECR—which already requires Scope 1 and 2 emissions (ie. everything but Scope 3, which covers supply chains). But as the targets and KPIs from questions 7 and 8 will increasingly involve reductions to Scope 3 emissions, it’s best practice to begin measuring and including this extra data early.

FCA - Financial Conduct Authority

What it is

The UK government has a broad goal of making TCFD-style disclosures the bare minimum across the British economy by 2025. While CRFD (see above) uses a slightly modified version, the FCA just requires a standard TCFD report each year (with one addition, covered below).

While the FCA has also discussed adding further requirements to this programme to make it a UK equivalent of the EU’s SFDR regime (see first section above), this discussion has been pushed to at least autumn 2022—and may be revisited by the new UK government.

What you need to know

In July the FCA published a review of the first batch of TCFD reporting from listed firms (summary here), in which it called for far more detailed reporting. Their position can be boiled down to “answer all the questions, fully, using the most precise data available”. While the FCA has been lenient with early filings, they’ve signalled a much more stringent approach going forward—mapping to what we cover here.

They’ve also broken out slightly different rules for three distinct constituencies: (1) standard listed firms, (2) premium listed firms, (3) asset managers and owners.

Standard listed firms

By rule, firms only have to state in their Annual Financial Report whether and where they’ve shared their TCFD disclosures (preferably in said report). While they have the right to opt out, to only address the disclosures in part, and/or to disclose them elsewhere, the FCA has been clear that these sidesteps now require strong justification—along with a credible plan to get on board.

These disclosures must also now include Scope 3 emissions—ie. from supply chains, unless said emissions are so small as to be “immaterial”. This is applicable as of accounting periods beginning on or after 1 January 2022—ie. for all reports in 2023 and thereafter.

Premium listed firms

The rules here are the same as above, with the exception that the programme’s effective date was 1 January 2021. All that’s changed since is updated guidance from TCFD itself (late 2021)—most notably in the requirement to include all material Scope 3 emissions.

Asset managers and owners

The FCA started with the largest organisations here: asset managers with over £50bn under management, and asset owners with over £25bn—who were asked to publish a pair of TCFD reports each year in a prominent place on their websites:

- An entity-level report, covering how they manage their own climate risks and opportunities on behalf of clients and consumers

- A product or portfolio report, covering disclosures for the investments themselves

These new disclosure requirements applied from 1 January 2022 on a calendar-year basis, with an initial reporting date of 30 June 2023. This date aligns it with SFDR filings, as many entities are subject to both programmes. Though the inclusion of Scope 3 “financed emissions”—ie. fair shares of emissions from assets—won’t become mandatory until 2024 filings.

These requirements are also now expanding to smaller firms on a yearly basis. Managers and owners with £5bn or more in assets must follow suit by 30 June 2024—though the FCA encourages them to join their larger counterparts in filing in 2023.

DWP - Department for Work and Pensions

What it is

DWP’s programme is also part of the UK’s larger push towards TCFD-style disclosures across the economy—starting with the largest organisations. Trustees of covered pension funds must soon publish an annual report that’s a slight riff on TCFD.

Note that this programme does not apply to Northern Ireland.

What you need to know

A core section of the report is “metrics and targets”, which requires trustees to calculate:

- The “financed emissions” of their fund—ie. their proportional share of the emissions from the companies and assets they’ve invested in. This ought to be calculated using “The Standard” created by the Partnership for Carbon Accounting Financials (PCAF).

- Their absolute emissions—i.e. financed emissions + direct emissions, expressed in megatonnes of CO2

- Their emissions intensity, which relativises absolute emissions by comparing them to the total value of the fund’s investments.

- One additional climate change metric (from this list)—the most straight-forward and useful of which is “data quality”, or the proportion of the portfolio for which emissions data was included. (Driving this number up to 100% has positive cyclical effects.)

The resulting report must be published on a free-to-access website, within seven months of each pension’s year end.

Each fund’s first compliance date is determined by when they reached certain thresholds in total assets or authorised master trusts (less expected payouts for that accounting year):

- £5bn+ on or after 1 March 2020 = their first report must be released within seven months of the end of the first accounting year that began on or after 1 October 2021

- £1bn+ on or after 1 March 2021 = their first report must be released within seven months of the end of the first accounting year that began on or after 1 October 2022

- £1bn+ on or after 1 March 2022 = their first report must be released within seven months of the final day of that accounting year + 366 days

- DWP has announced consultations for 2024 to evaluate lowering the thresholds to capture smaller funds—who right now have no coming requirement

If a fund’s assets fall below £500m, the trustees must submit a final report for that accounting year. Trustees are also allowed to exclude financed emissions data—also known as Scope 3— in their first reporting year, though they’re encouraged to measure and report what they can.